Life is full of surprises, some exciting, some expensive. Whether it’s an unexpected home repair or a spontaneous travel opportunity, having an emergency fund savings plan ensures you’re financially ready for anything.

This guide is for you if you’re wondering:

✓ How much should I save in an emergency fund?

✓ What are the best places to keep an emergency fund?

✓ How do I start building an emergency fund with low income?

✓ Where do I invest an emergency fund for security and growth?

✓ How long should an emergency fund last?

✓ How do I create a plan to grow my emergency fund?

If these questions are on your mind, you’re in the right place. Let’s explore the steps to creating and maintaining an emergency fund effectively.

Why is an emergency fund important?

An emergency fund savings plan protects you from financial setbacks that can arise without warning. Unpredictable expenses can disrupt your budget if you do not have money set aside. Without an emergency fund, many people rely on credit cards or loans, which can lead to long-term debt and financial stress.

Having an emergency fund for financial security means you can handle urgent costs without borrowing money. For example, if your car breaks down, you can pay for repairs immediately instead of using a credit card with high interest. If you face a sudden job loss, savings can cover your rent and bills while you search for new employment.

An emergency fund also provides financial flexibility. If a great opportunity arises, such as a job offer in another city, having savings allows you to relocate without financial strain. If you need to take time off work for personal reasons, a well-funded emergency account ensures you can manage expenses without worrying about lost income.

> Learn more about risk diversification and financial security

How much should you save in an emergency fund?

The right amount for your emergency fund savings plan depends on your income stability, expenses, and financial obligations. If saving several months’ worth of expenses seems overwhelming, start with a smaller goal.

Once that milestone is reached, continue adding to your fund over time. Even a modest emergency fund provides a financial cushion that prevents reliance on high-interest debt during unexpected situations.

> Find out how to set realistic financial goals

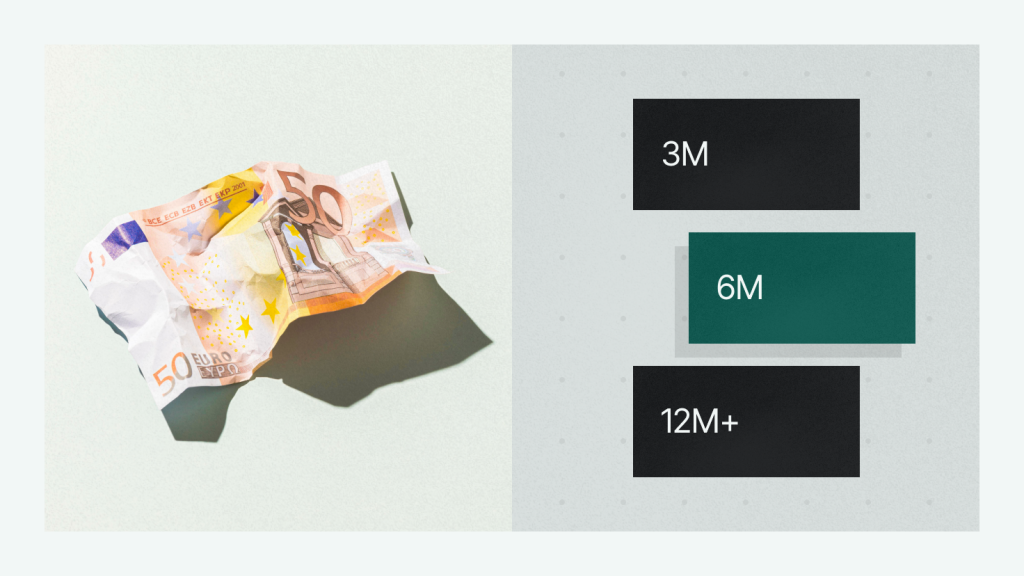

How long should an emergency fund last?

The amount of time your emergency fund should cover depends on your income stability, job security, and financial responsibilities. While the general recommendation is three to six months of essential expenses, some situations may require a larger safety net.

- Three months – Suitable for individuals with stable, salaried jobs and minimal financial obligations.

- Six months – Ideal for freelancers, business owners, or those with variable income. A larger fund helps manage unpredictable cash flow.

- Twelve months or more – Recommended for retirees, individuals with high financial commitments, or those in industries with uncertain job stability.

If you need to use your emergency fund, focus on stretching your savings by reducing discretionary expenses and prioritizing essential costs. Once your financial situation stabilizes, replenishing your emergency fund should become a priority to maintain long-term security.

> See how to create a smart asset allocation strategy

Steps to start an emergency fund

Building an emergency fund requires planning, discipline, and small, consistent steps. The following emergency savings strategies can help you reach your goals efficiently:

1. Set a clear savings goal

The first step in creating an emergency fund savings plan is deciding how much you need. To determine your savings goal, start by calculating your monthly essential expenses, including rent or mortgage, utilities, groceries, insurance, and loan payments. Multiply this by the number of months you want to cover.

Using an emergency fund calculator can help estimate the right target based on your financial situation.

2. Open a separate account

Where you keep your emergency savings matters. If you leave the money in an account that you use frequently, you might spend it without realizing it. The key is to balance liquidity and security. Your emergency fund should be easy to access but separate from daily spending.

3. Automate your savings

One of the most effective emergency savings strategies is automation. Set up a recurring transfer from your paycheck or checking account to your emergency fund. Automating your savings helps you stay consistent without having to think about it. Even a modest amount saved regularly adds up over time, bringing you closer to your financial goal.

> Find out how to automate your investments after securing your savings

4. Start small and increase over time

Building an emergency fund is a process, and every step forward strengthens your financial security. Set an initial savings goal that feels achievable, then keep adding to it over time. Reaching your first milestone, whether it’s €100, €1 000, or €10 000, creates a foundation for handling unexpected expenses. From there, continue growing your fund by saving a percentage of your income regularly.

5. Cut unnecessary expenses

Finding extra money to save may require adjusting your spending habits, by identifying areas where you can reduce non-essential costs.

By following these steps to start an emergency fund, you’ll create a financial buffer that protects you from unexpected costs and provides greater financial stability.

> Discover low-risk investment strategies for your savings

Best places to keep an emergency fund

Where you store your emergency savings affects both the security and accessibility of your money. The ideal account should keep your money safe, allow quick withdrawals when needed, and provide some interest to prevent inflation from eroding its value.

High-yield savings accounts

A high-yield savings account is one of the best accounts for emergency savings because it offers easy access while earning more interest than a standard savings account. Funds are insured, typically up to a limit of €100 000, and can be withdrawn at any time without penalties.

When comparing an emergency fund vs. savings account, the key difference is in its purpose. A general savings account is often used for planned expenses, such as vacations, home upgrades, or large purchases. An emergency fund, however, should be kept in a separate account, designated only for unexpected financial needs.

This separation prevents accidental spending and helps you maintain financial security when unexpected expenses arise.

Money market accounts

A money market account combines the benefits of a savings account with limited checking features. It typically offers higher interest rates than regular savings accounts and allows easy withdrawals, making it a strong option for an emergency fund.

Short-term Certificates of Deposit (CDs)

A short-term CD provides higher interest rates than standard savings accounts, but your money is locked in for a set period, such as three to six months. If you don’t need immediate access to all of your emergency savings, keeping a portion in a CD can help grow your funds while maintaining security.

What to avoid

Avoid storing your emergency fund in high-risk or illiquid assets such as stocks, real estate, or long-term investment accounts. These options may offer higher returns, but their value can drop during market downturns, making it difficult to access your money when you need it most.

Choosing the best places to keep an emergency fund ensures that your savings remain accessible, protected, and steadily growing.

How to build an emergency fund fast

If you need to save quickly, focusing on smart financial habits and small adjustments can help you reach your goal faster. Whether you are starting from zero or trying to grow your existing fund, these strategies can accelerate the process.

1. Increase your income

Finding ways to earn extra money can make a significant difference. Taking on freelance work, selling unused items, or starting a side hustle are effective ways to boost savings. Even small additional income streams can help you build your emergency fund faster.

> Check out side hustle ideas to boost your savings

2. Reduce non-essential expenses

Reviewing your spending habits and cutting unnecessary costs frees up money for savings. Canceling unused subscriptions, cooking at home instead of dining out, and negotiating lower bills can create extra room in your budget to put toward your emergency fund.

3. Prioritize savings

Treating your emergency savings like a fixed expense, just like rent or utilities, makes it easier to stay on track.

4. Use windfalls wisely

Unexpected money, such as tax refunds, bonuses, or cash gifts, provides a great opportunity to grow your savings. Allocating a portion of any financial windfall directly to your emergency fund will help you reach your goal more quickly.

5. Make temporary lifestyle adjustments

Short-term sacrifices can lead to long-term financial security. Cutting back on discretionary spending for a few months—such as skipping expensive entertainment or delaying non-essential purchases—can help you reach your savings goal sooner.

Emergency fund vs. investments

Many people wonder whether they should focus on building an emergency fund for financial security or start investing for long-term growth. Both are important financial strategies, but they serve different purposes and should be approached separately.

Key differences between an emergency fund and investments

An emergency fund is meant to cover unexpected expenses such as medical bills, car repairs, or temporary job loss. It needs to be:

- Safe – The value should not fluctuate with market conditions.

- Liquid – You should be able to withdraw the money immediately when needed.

- Separate from investments – It should not be tied to assets that could lose value.

Why investments are not a substitute for an emergency fund

Investments are an essential part of building long-term wealth. They help grow your money over time and can be used for major financial goals such as:

- Retirement – Investing in stocks, ETFs, or mutual funds helps grow wealth for financial independence later in life.

- Buying a home – Investments can provide returns that help fund a down payment or other large purchases.

- Funding education – Long-term investments can support education costs for yourself or your family.

Once your emergency fund is in place, you can begin investing confidently, knowing that you have a financial cushion to handle unexpected situations.

> Explore the best short-term investment options for liquidity and returns

Building a balanced investment portfolio

Once your emergency fund savings plan is in place, you can focus on growing your wealth through investing. A well-diversified portfolio helps balance risk and return, ensuring your money works for you over the long term.

Investment options on Mintos

- Loans – Earn regular interest payments, diversify across sectors and regions, and choose between automated or hands-on investing.

- Bonds – Invest from €50, earn fixed returns, and diversify your investments. A great option for those looking for steady, passive income.

- Passive real estate – Generate monthly rental income from property-backed investments with a lower entry point than direct ownership.

- Smart Cash – Access a money market fund with the highest rating that offers higher interest than traditional savings with same-day withdrawals.

- ETFs – Invest in ETFs globally with a single portfolio, enjoy diversification, and zero commission fees, starting from just €50.

Disclaimer

This is a marketing communication and in no way should be viewed as investment research, advice, or a recommendation to invest. The value of your investment can go up as well as down, and you may lose part or all of your invested capital. Past performance of financial instruments does not guarantee future returns. Investing in financial instruments involves risk; before investing, consider your knowledge, experience, financial situation, and investment objectives.

Any scenarios or examples provided are for illustrative purposes only. They do not guarantee specific outcomes or returns and should not be relied upon when making investment decisions. Actual results may vary based on market conditions, issuer performance, and other factors.